The council judgement classifies Lammhults as a conditional small-cap turnaround with microcap trading risk. That is the cleanest label. The company has sufficient substance to justify serious work: established brands, meaningful sales, a listed reporting framework, no obvious rescue-financing pattern, a credible Library signal and a valuation that can move sharply if EBIT normalizes.

But the company also has enough weakness to punish lazy optimism. Office is too important to ignore. Q1 adjusted EBIT was too weak to underwrite the long-term margin target. Working capital can move equity value. Net debt is material. Share structure and concentrated control reduce minority influence. Low trading liquidity raises the required margin of safety.

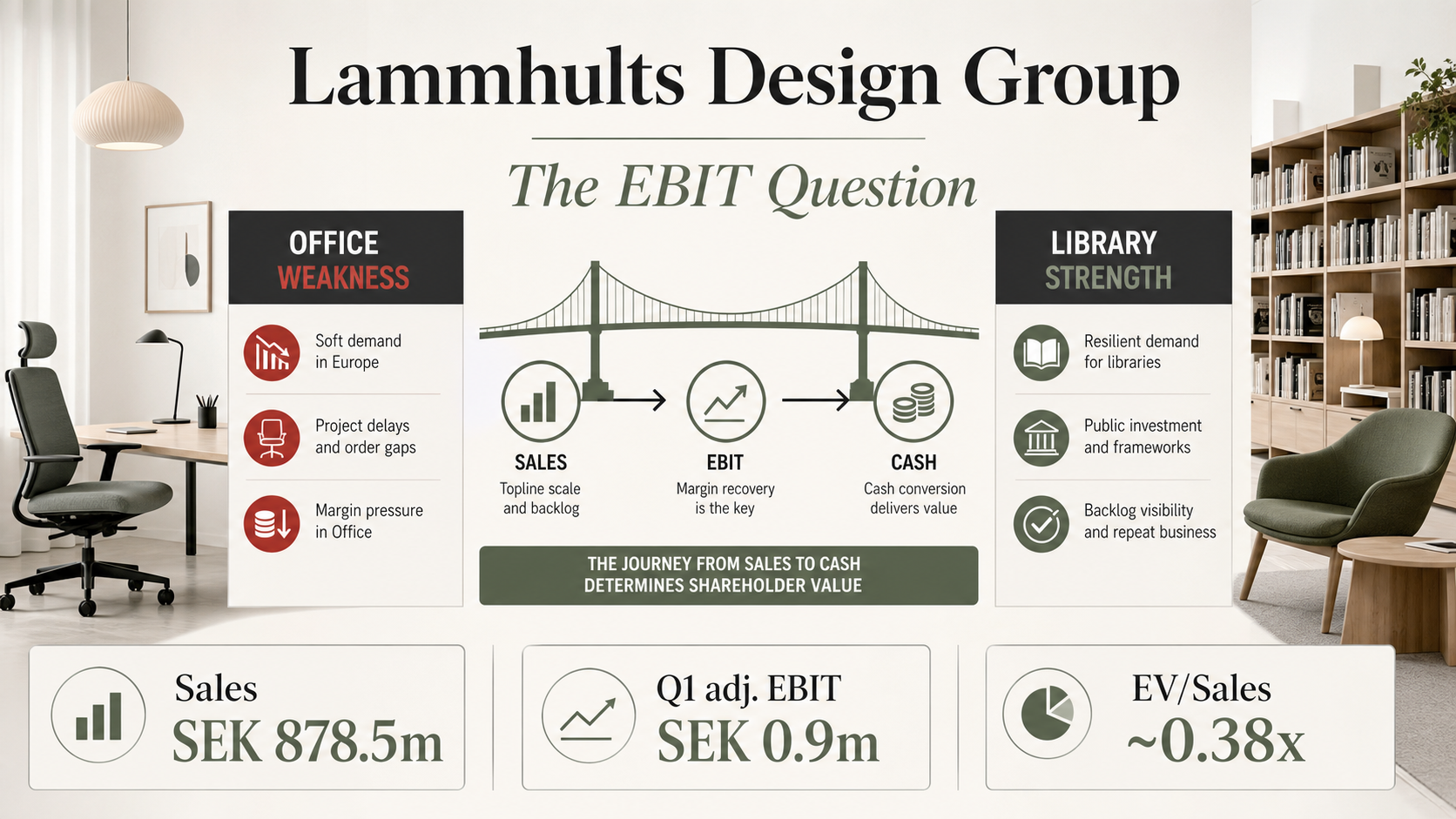

The investable version of the case needs evidence: Office order intake stabilizing, Library backlog converting profitably, adjusted gross margin holding around 36-37%, reported EBIT moving with adjusted EBIT, free cash flow returning and net debt falling. Without that, EV/Sales at 0.38x is not a bargain; it is just a number dressed up as a thesis.

Position sizing should follow that uncertainty. A small, patient investor can treat Lammhults as an evidence-driven recovery position, provided the maximum loss and slow exit are acceptable before the first share is bought. A larger investor may find the idea intellectually attractive but economically awkward because the liquidity does not support meaningful scale. That does not make the thesis wrong. It means the implementation has to respect the actual market in the share.